It may not have grabbed the limelight like ChatGPT and rotisserie air fryers, but debt capacity was one of the hot topics of the past year.

The reason? Soaring interest rates, which caused many business leaders to take a fresh look at the amount of debt on their balance sheets. Companies with high debt levels found that interest expenses were devouring their cash flow.

Loans come in many forms, from short-term lines of credit to long-term borrowing. But no matter how you approach debt financing, you always have to consider one thing: will you be able to service your debt without risking your company's survival?

Lenders ask that question too. They will estimate your debt capacity, look at your outstanding loan obligations, and use this information to make a decision.

In this guide, we'll talk about how debt capacity (also known as borrowing capacity) works, how to calculate your debt capacity, and what it means for your ability to borrow.

What is debt capacity?

Debt capacity is the level of borrowing that a business can sustainably manage. If you borrow more than your capacity, it could jeopardize your future financial stability.

Debt capacity calculations vary greatly depending on the nature of your business and the purpose of the loan. While lenders will assess your debt capacity based on your full financial position, they usually focus on one of two things:

- Cash flow: Generally, this means your Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA). For senior debt (also known as traditional bank debt, first lien), your debt capacity is typically three times your EBITDA.

- Assets: Some lenders will focus on your existing net asset value when assessing your debt capacity. If you're borrowing to fund an asset purchase, such as a commercial real estate acquisition, then the lender may include the value of the target asset in their calculation.

Of course, cash flow and assets both play a role in any lending application. However, lenders will take one of the above approaches to debt capacity depending on the nature and purpose of your loan.

Debt capacity alone does not guarantee how much your business can borrow. Even if you're well within debt capacity limits, you'll still need to meet other relevant lending criteria and are subject to bank-specific underwriting criteria

Debt capacity based on cash flow vs assets

Your circumstances play a big part in how lenders assess debt capacity. For example, if you're running a startup with limited cash flow, lenders can consider the value of your assets. Generally, debt capacity is often related to the loan term. It works like this:

- Short-term loans: You may require a bridge loan, line of credit, or another type of financing that can help you with short-term capital needs. In this scenario, lenders want to know they have security if you can't meet your obligations. For this reason, they will often take an asset-based approach to debt capacity.

- Medium-term loans: If you require more strategic lending options, such as debt financing for expansion or acquisition, then lenders will focus on your ability to make regular repayments over time. This means a cash flow-based approach, which may include potential revenues from your future growth.

- Long-term loans: When borrowing for real estate purchases or other long-term commitments, lenders will again take an asset-based approach, which may include the market value of your new asset. These are general guides and can vary depending on your industry and your business strategy. The key takeaway here is that lenders want to help you grow and understand that each business has unique needs. Debt capacity is about ensuring they lend in a fiscally responsible way, reducing risk for themselves and you.

How to calculate debt capacity

Debt capacity calculations can vary in different circumstances. Some lenders might look at your current cash flow levels when assessing your debt capacity, while others might look at your assets or the value of an asset you wish to purchase.

You can get an idea of your business's debt capacity if you understand some fundamentals, including the following:

Earnings Before Interest, Tax, Depreciation and Amortization (EBITDA)

EBITDA is essentially your operating profit, but without deductions for capital expenditure. Lenders consider this the most accurate representation of your cash flow and, therefore, your ability to service your loan.

Senior Debt capacity is generally calculated at 3x EBITDA, although this can vary and does not guarantee your ability to borrow.

Current debt position

Lenders want to know how much of your debt capacity is available, which means looking at your current outstanding loans and repayment schedules. Depending on circumstances, they may consider:

- Gross debt: The total of all outstanding debt liabilities

- Senior debt: Debt owed to priority creditors, which is usually secured against an asset

- Interest: The cost of servicing your outstanding debts

Lenders generally prefer a Senior Debt to EBITDA ratio of 3:1, although this varies depending on factors like your company’s size, your growth plans and the industry in which you operate.

Total financing requirements

Lenders will often expect you to offer a downpayment, which can impact the total financing available to you. Some common scenarios include:

- Commercial real estate loans: Lending is often limited to 70%-80%, with borrowers expected to provide a 20%-30% downpayment

- Business acquisition loans: Lenders might not be willing to offer more than 50% of the acquisition price

These requirements can impact your overall debt capacity, especially if you intend to raise additional investment capital by liquidating assets, selling equity, or seeking additional debt financing.

Loan purpose and term

Businesses take out loans for any number of reasons, and these reasons can affect their ability to repay. For example, consider a thriving business that plans to acquire a strategically important competitor. While this might temporarily create a senior debt-to-EBITDA ratio greater than 3:1, the potential future growth could lead to a much higher EBITDA in the future.

Factors that lenders will look at when calculating your debt capacity include:

- Loan purpose: Do you need finance to support a well-developed business strategy? Or will you acquire a tangible asset, such as commercial property?

- Loan term: Long-term lending has lower risks, especially if your business has a stable track record. However, your capacity to service short-term debt might be more limited.

- Loan security: Collateral gives lenders some peace of mind, so they may take a more lenient approach to debt capacity if you can support the loan with assets.

Remember, debt capacity is intended as a guide to whether your debt will be sustainable. It's up to you, your finance team, and the lender to determine if a loan is prudent.

Industry-specific variables

Debt capacity also varies across different sectors. Some industries are naturally high-risk, and lenders may calculate a lower debt capacity. Other sectors are highly leveraged, and lenders understand that your business requires access to capital above normal debt capacity limits.

The Risk Management Association offers some data on how each industry works. Lenders also consider factors such as:

- Cyclicality: Sectors producing essential goods and services, such as utilities and healthcare, remain comparatively stable even during economic downturns. Industries that are more vulnerable to downturns include construction and financial services.

- Barriers to entry: Industries like tech have low barriers to entry, meaning that a disruptor could threaten your market position at any moment.

- Industry growth rate: Growth will affect your ability to service loans in the long run. High-growth industries like finance have a naturally higher debt capacity.

All these factors are risk elements, and lenders want to limit their exposure to risk. Lenders will be more open to offering finance if businesses in your industry have a good track record for repayments.

FAQs

What is debt capacity in business?

Debt capacity is the amount of debt a business can safely take on. Companies with spare debt capacity can look at borrowing to fund their strategic goals. However, businesses close to their debt capacity limit should consider whether they can meet their obligations, especially if they experience a downturn.

How much debt should a company have?

In general, companies should aim to borrow senior debt at most three times their EBITDA. Your EBITDA is your operating profit without deductions for tax, interest, depreciation or amortization.

However, in practice, some businesses may need to exceed this amount. If so, then lenders will look at asset values and your current debt obligations. Some lenders may calculate your senior debt capacity at less than 3x EBITDA.

Also, it's good practice to stay below your total debt capacity. This gives you some breathing room in case you need to borrow more or if a downturn makes it harder to service your current debts.

How can I calculate debt capacity?

The easiest way to look at senior debt capacity is to work out your EBITDA, which is Earnings Before Interest, Tax, Depreciation and Amortization. The rule of thumb is: senior debt capacity is three times your EBITDA.

However, debt capacity is not always calculated in the same way. Different lenders will look at different things, including the nature of your existing debts and your total asset value. They'll also factor in your business plans and the nature of your industry.

Also, note that debt capacity does not guarantee a loan. Lending is always subject to approval, regardless of your notional capacity.

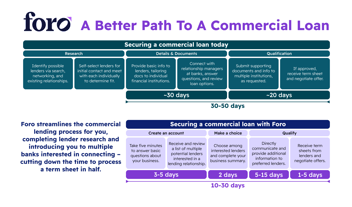

How Foro can help you find the right lending partner

Debt capacity can sometimes be a roadblock for businesses. Because there are so many ways of calculating capacity, you may sometimes struggle to convince your local lender that you can make repayments.

Foro can help. Our powerful A.I. engine will study the details of your application and quickly match you with a lending partner that understands your strategy.

Still running into problems with debt capacity? No problem — if you can't find a match, Foro has an experienced team that will work with you directly to help you figure out the best path forward.

Plus, Foro Capital Markets can help raise junior debt or equity, allowing you to fill out your capital stack in one place. Set up your business profile right now, or get in touch and we’ll answer any questions you may have.

-Jan-03-2024-02-44-48-9464-PM.png?width=1000&height=187&name=Blog%20CTA_1000%20%C3%97%20187%20px%20(7)-Jan-03-2024-02-44-48-9464-PM.png)

About The Author: Ber Leary

Ber Leary worked in investment management for over ten years. He's now a full-time content marketing consultant specializing in finance technology and management strategy. Connect with Ber on LinkedIn.