Not a great time to launch a new construction project, you might assume. But if that’s the case, why are so many contractors fully booked? And why are so many city skylines bristling with cranes?

The truth is that some parts of the construction industry are down, while other sectors are thriving — and some are busier than ever.

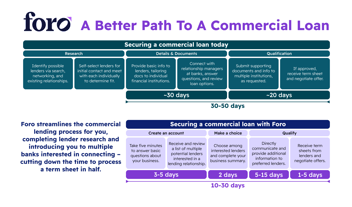

Economic turbulence can make it harder to find commercial construction financing, but financing is out there. In this guide, we'll talk you through the essentials of commercial construction loans and finding the right lending partner for your next project.

Who needs a commercial construction loan?

Commercial construction projects generally fall into three categories:

- Owner-occupied: A project where you retain 51% or more occupancy of the finished building

- Non-owner-occupied: Projects that you intend to rent or sell the majority upon completion

- Redevelopment: Major changes to an existing commercial property, such as extensions, redevelopments or repurposing

If you're planning any building work for commercial purposes, you could be eligible for a construction loan.

How commercial construction loans work

Most lenders understand that commercial construction works in two phases. First comes the building phase, during which you must pay cash for contractors, materials, and all other costs associated with an ambitious construction project. In this first phase, you need readily-available capital on flexible terms.

Then comes the realization phase. Non-owner occupiers rent or sell the new property in this phase, while owner-occupiers will start operating from the new space. In both cases, this is the point where you begin to earn income from your new investment.

To reflect this two-stage process, commercial construction loan products are often structured in two phases:

- Interest-only period: During the initial loan period, you only need to service interest payments. Lenders may offer you a draw schedule, which provides you access to capital after you hit certain project milestones. Ideally, the interest-only period will end when your project is complete.

- Term loan: Once your building is finished, you begin repaying the principal. This might often be structured as a mortgage-style term loan, although other structuring options are available.

The most important thing in commercial construction borrowing is to ensure all building work is complete before the end of the interest-free period.

In practice, this can be tricky. Construction projects often take much longer than the initial estimates, especially if you hit unavoidable roadblocks like lousy weather or supply shortages. That's why it's so important to seek a lender with terms that suit your needs. If possible, try to allow some extra breathing room at the end of the interest-free period to account for project delays.

Maximum value of a commercial construction loan

Construction is a significant investment, and commercial property development comes with a hefty price tag. Fortunately, the lending market can support this kind of ambition, although the amount you can borrow depends on the nature of your project.

The first thing to note is that lenders have two formulas for calculating how much you can borrow:

- LTC (Loan-to-cost): The total cost of construction

- LTV (Loan-to-value): The value of the completed property

The value of a property, as determined by an appraisal, is used to calculate the loan-to-value ratio (LTV) for completed properties. On the other hand, in-progress construction projects are evaluated based on their project budget, which is known as the loan-to-cost ratio (LTC). If both LTV and LTC are calculated by your lender, the lower value will be used to determine your loan eligibility.

Most loans are limited to 80% of either LTV or LTC, and a down payment of 20% is typically required. However, if your lender has concerns about your project's profitability, they may require a larger down payment.

Types of commercial construction loans

Commercial construction loans are often a combination of two different types of loan: one for the interest-only period, followed by a term loan. Here are some of the options that may apply:

Commercial line of credit

Lines of credit offer flexible access to capital, which you can withdraw and repay during pre-agreed windows. Your debt servicing obligations are interest-only, with more flexible terms for capital repayments.

When using a line of credit for construction, you may need to agree on a draw schedule with the lender. This schedule divides your loan into smaller amounts, each becoming available after you hit certain milestones. Some of these milestones may involve a site inspection to confirm that the project is on track.

Bridge loans

Bridge loans are short-term, high-interest loans with a balloon payment at the end. If you can't find a construction loan or commercial line of credit, this might be one option to get your project started, although you will most likely need a term loan to cover the final payment.

In some cases, developers may use bridge loans to handle unexpected issues, such as the interest-free period ending before the building is complete. However, this approach is not ideal, which is why it's so important to find a construction loan partner that offers terms suited to your needs.

Term loan

Once the building work is complete, your borrowing may convert to a term loan. A term loan is an agreement to repay the principal over an agreed period, with interest that may be fixed or variable.

Term loans are secured against assets, so if you default, then you may lose your new property. That's why it's so important to ensure that your interest-free period gives you enough time to finish all construction.

SBA loans

Small Business Association loans can be used for commercial construction projects. Most borrowers go through the SBA 7(a) program for this kind of financing, although Foro can also help you find SBA 504 loans, which are intended for major capital investment projects.

SBA-backed borrowing has one major advantage: smaller down payments. While most commercial construction lending requires a minimum down payment of 20%, SBA loans can require as little as 5%. That difference can be a game changer for growing companies when making large cash outlays such as for project development.

Lending requirements for commercial construction loans

The commercial construction loan process tends to be quite document-heavy. Lenders will ask for extensive paperwork, including:

- Appraisal: An up-to-date appraisal is essential to the commercial construction loan process. Commercial lenders will insist on an appraisal performed by one of their consultants or an approved third party.

- Environmental report: Lenders also insist on an environmental report before proceeding. A basic Phase 1 report will assess whether the property has any existing environmental contaminants or concerns. If so, then you may require a more detailed analysis.

- Feasibility study or market analysis: For non-owner-occupied projects, lenders will want to see that your project is financially viable. For example, if you're building rental accommodations, you need to show that the local rental market can support your business plan.

- Construction Budget: You'll need a detailed breakdown of the total project cost, including fees. This will form the basis of an LTC analysis, which determines how much you can borrow.

- Contracts: You should have confirmed agreements with your general contractor, subcontractors, architects, engineers, and anyone else involved in construction. This will also help you provide an accurate cost analysis.

- Financials: Lenders may also require financial analysis, such as cash-flow projections. This will help them determine if you can service the loan.

If this process sounds complex, time-consuming, and potentially stressful, that’s because it traditionally has been. The Foro philosophy is that it doesn’t have to be this way. After you’ve spent five minutes or less filling out a guided business profile, we’ll be there to support you in every phase of the journey toward your construction loan approval.

Who pays commercial construction loan fees?

Providing lenders with the documentation they need can be expensive, as you'll need to pay surveyors, analysts, consultants and others to produce reports. This is on top of other expenses, including legal and closing costs.

Fees and report costs are your responsibility, but you may be able to bundle the cost into the overall loan. Speak to potential lenders to see how they can assist you with fees and other expenses. Again, Foro’s team of industry experts can help you navigate these and other conversations.

Alternatives to further commercial construction loans

Construction loans are just one way of securing funding for your next project. Other options include:

Equity financing

Equity financing allows you to raise capital without making any future repayments. You sell shares in your company, either through a private sale or on an investment market, and the incoming capital goes towards your project.

If you choose this option, keep in mind that you’re bringing in an investor. They will have some say in the project, which dilutes your overall control. They will also be entitled to a share of future profits, which could end up costing you more than debt-based commercial construction financing.

Mezzanine financing

Mezzanine financing is a hybrid of debt and equity financing. A mezzanine loan works like a regular term loan except that it is secured against equity. If you default on your loan, then the lender assumes control of the equity and dilutes your control.

However, if you repay the loan on time, your debt is cleared, and you retain all equity. Mezzanine loans can offer a great deal of flexibility, especially if you're struggling to find a traditional term loan. However, because mezzanine financing is a junior loan (i.e. the holders can only claim their share of a company’s assets after the senior lenders have been repaid), it’s considered riskier than other forms of financing. As a result, mezzanine loans tend to carry higher interest rates.

Frequently Asked Questions

What can you use a commercial construction loan for?

Commercial construction loans are suitable for any investment in new or existing property development. This can mean creating a new location for your business or building commercial property that you intend to sell or rent. You can also borrow to cover the cost of constructing housing or apartment blocks.

You don't need to build a brand new property — you can use a commercial construction loan for work on an existing property. Any project that involves extensive commercial building work is a candidate for this type of loan.

Can you refinance a commercial construction loan?

You can refinance a commercial construction loan, although how you do so will depend on your project's current state. If you're in the interest-only period, refinancing can be difficult as it often means that something has gone wrong. Talk to your current lender or consult Foro's advisers before seeking an alternative arrangement, such as a bridge loan.

After that, you're simply refinancing a term loan. As with any debt restructuring, it's a matter of looking around for a lender that can accommodate your needs. Again, Foro can help you find the right partner for refinancing your commercial construction loan.

What percent down payment is needed for a construction loan?

Down payments are calculated based on the lower of the LTV or LTC advance rates offered by the lender. For example, if the lender offers 80% LTV and 75% LTC, the client will be expected to put up 25% as a down payment.

In the case of an SBA-backed loan, your up-front payment could be as low as 5%. Use Foro’s loan matching service to see if you're suitable for an SBA loan.

-Jan-03-2024-02-44-48-9464-PM.png?width=1000&height=187&name=Blog%20CTA_1000%20%C3%97%20187%20px%20(7)-Jan-03-2024-02-44-48-9464-PM.png)

About The Author: Ber Leary

Ber Leary worked in investment management for over ten years. He's now a full-time content marketing consultant specializing in finance technology and management strategy. Connect with Ber on LinkedIn.