-----

Sometimes, it’s not you. It’s the economy.

Even companies with solid track records and strong growth potential may find financing harder to come by during periods of economic volatility. When conditions such as higher interest rates, inflation, and sagging consumer confidence sap the economy’s momentum, lenders naturally become more cautious. “Just because you can afford to repay a loan at the going rates doesn’t mean every bank can afford the risk,” says Will Howard, head of Relationship Management at Foro. “As risks rise, they’re going to be more conservative. What they were approving yesterday, they may not be approving today.”

Fortunately, while willing lenders may be harder to find, they are out there, Howard says. These suggestions could help you find them.

1 – Hang in there. When economic conditions begin to deteriorate, you may feel like giving up the search for financing until things improve. “In the long run, that’s not going to be a good decision for your business,” Howard believes. Forgoing capital you need could mean delaying growth or turning down customers that, once gone, may never return. Just as important, demonstrating your ability to repay loans through times of adversity is essential to building your reputation. “That lends to your company’s credibility and credit quality when conditions improve.”

2 – Expand your search. Don’t read one or even a handful of rejections as a blanket dismissal, Howard advises. “You may walk away wondering ‘Why am I not financeable?’ when the real problem is that the banker you spoke with has received instructions from the credit officers in the organization not to lend to your industry.” As economic conditions tighten and major banks become more conservative, “Some smaller banks may stay aggressive because they’re trying to grow market share,” Howard says. These opportunities may be with lenders in your town or city, or some other part of the country entirely.

3 – Speak with lenders who know your industry. Lenders unfamiliar with your industry could exaggerate your risks while overlooking key opportunities. During the pandemic, for example, while many businesses suffered, home improvement companies thrived as millions of Americans focused on sprucing up their homes. Even if your industry is struggling, a lender who understands the landscape may appreciate that while your sales are temporarily depressed, you’re outperforming your competitors and are hence a good risk, Howard believes. Bottom line: “There's probably a community or regional bank somewhere that has a commercial team specializing in your area that would be eager to lend to a company like yours.”

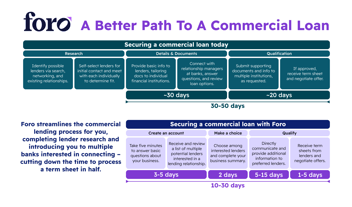

4 – Tap the power of technology. OK, so lenders are out there – but how do you find them when engaging one at a time proves to be a time-consuming disappointment? Foro’s proprietary technology uses artificial intelligence to pair you with companies in your area or around the country most likely to be interested in lending to a business such as yours. “As economic conditions change, we have live data recognition that tells us who is staying active and still doing deals,” Howard says.

Instead of repeatedly engaging banks on an individual basis, businesses provide information on a single, standardized form. Foro then checks this information against a nationwide network of commercial banks to find lenders that have expressed an interest in similar businesses. Banks and other lenders pay for the service, which is free to businesses. “We know the markets and industries,” Howard says. “We can introduce you to several lenders who are active and interested.”

5 – Explore government loans. Whether you’re looking for a term loan, real estate loan, or a business line of credit, the federal Small Business Administration (SBA) offers solutions that may be particularly attractive when economic conditions deteriorate. “During a downturn or recession, the SBA is huge,” Howard says. Borrowers still work with traditional financial institutions such as banks or credit unions, but the SBA backs a significant portion of the loan in case the borrower defaults. “They take a lot of risk and uncertainty off the lender's plate,” he adds. Another option: the USDA also offers similar loans, designed especially for companies in rural areas.

Government loans come with restrictions and may involve more paperwork and processing time than a traditional commercial loan, Howard notes. And, if you own 20% or more of the company, you’ll have to provide a personal guarantee. During a stronger economy when banks are more aggressive and confident, a traditional commercial loan could be the way to go. Yet it’s always a good idea to at least consider government loans, Howard notes. A Foro representative can help you understand the choices and help you make the best decision for your situation. For more on SBA and other loans, see Foro’s overview here.

6 – Consider alternative financing. After years of historically low interest rates, recent sharp hikes by the Federal Reserve to counter inflation revealed a painful truth: rising rates make borrowing more expensive. “At some point, businesses may find that equity financing is actually more attractive than debt.” Unlike loans, which are repaid with interest based on prevailing rates, equity financing comes from investors who in return receive partial ownership. Another advantage: While traditional financial institutions may require that loans be used for specific, agreed-upon purposes, equity financing offers the flexibility to put the money where it’s most needed, Howard explains.

Among the tradeoffs, selling equity means sharing the rewards when the business takes off or is sold. Moreover, investors with even partial ownership may want a voice in key business decisions. Equity deals are complex and should only be undertaken with the help of experienced advisors, Howard says. Foro, for example, can walk you through the pros and cons, and help you determine what mix of debt and equity might be right for your business. And, if you move forward, Foro can work with you to structure the deal.*

7 – Use good times wisely. The economy, like the weather, is cyclical. When conditions change and the economy is strong, borrowing becomes easier. Use this time to weatherproof your finances for the next downturn or recession, Howard suggests. Two key areas to focus on are liquidity and its close cousin, cash flow. Liquidity refers to the amount of cash you have on hand right now to pay expenses. “Depending on the industry, lenders are usually looking for one to six months of liquidity,” Howard says.

Cash flow refers to the money regularly coming in from your customers or clients, and available to be paid out for expenses. “Here, lenders are looking for consistency,” Howard says. “They want to know what portion of your cash flows are going to be subject to major market volatility,” he says. “Long-term recurring customers with steady contracts are a good sign that your recurring revenue will continue. Otherwise, lenders may see you as a cash flow risk.” Even as you seek new customers, use good times to weed out those with spotty payment histories, and work to solidify relationships with your best customers.

Finally, be careful about the amount of leverage you assume, Howard suggests. Banks willing to lend you three or four times your earnings during good times might pressure you to accelerate repayments when conditions tighten. “If you’re highly leveraged, use the good times to proactively reduce or consolidate your debt,” Howard suggests. That way, when the economy turns, your payments may be smaller and you’ll have a record of responsible debt management that will appeal to lenders. See this FAQ page for more information what lenders are looking for from your company.

While there’s no guarantee when it comes to seeking capital, keep in mind that for most good companies, there’s a lender to be found, Howard says. A concerted approach, with the right tools, resources and partners can help give you the peace of mind of knowing your business can move forward, whatever surprises the economy holds in store.

Please visit Foro.io for more ideas on finding capital, for information on types of loans available to businesses like yours, to learn how a powerful search platform could transform your search.

* Equity services, unlike the search for lenders, involves a fee.

-Jan-03-2024-02-44-48-9464-PM.png?width=1000&height=187&name=Blog%20CTA_1000%20%C3%97%20187%20px%20(7)-Jan-03-2024-02-44-48-9464-PM.png)

About The Author: Charlie Slack

An award-winning business and financial writer, Charlie Slack is co-author (with Reed Phillips) of QuickValue: Discover Your Value and Empower Your Business in Three Easy Steps. (McGraw Hill, 2021). He is also the author of four mainstream books, most recently Liberty's First Crisis: Adams, Jefferson, and the Misfits Who Saved Free Speech (Grove Atlantic, 2015).